The war between Alipay and WeChat (which peaked a few years ago during epic Chinese New Year promotion campaigns) keeps raging. And data seems to support what everyone feels: WeChat is catching up fast.

The rise of WeChat

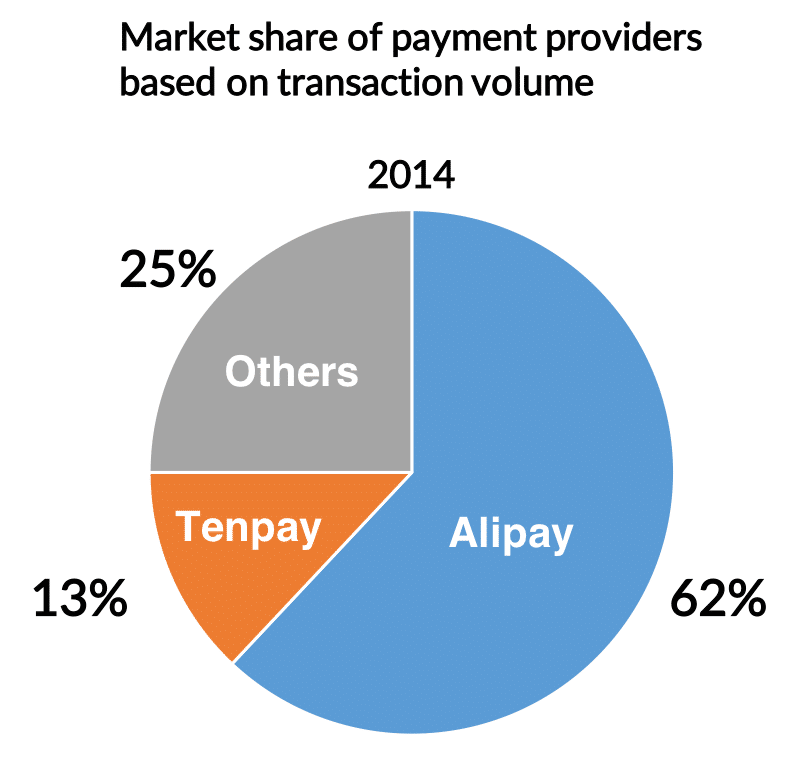

Although WeChat is a relatively newcomer to the online payment market (Alipay launched in 2004 – 7 years before the launch of WeChat, and 10 years before WeChat Pay!), but WeChat is quickly catching up with Alipay.

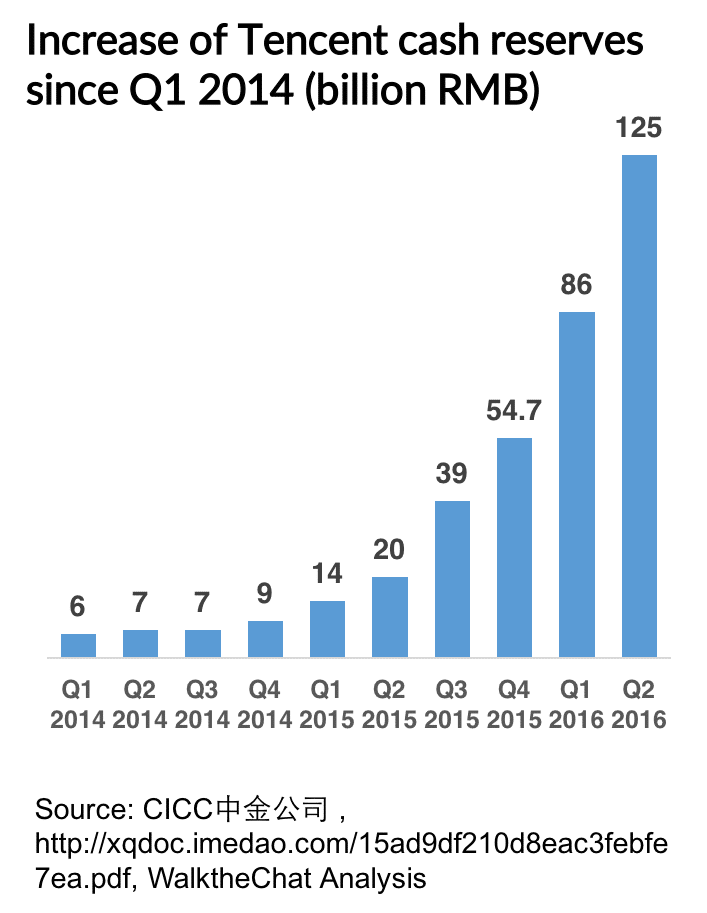

Another indicator is the reserves that Tencent (as a payment processor) has to justify to the Chinese government. These reserves have been growing exponentially since Q1 2014, suggesting that WeChat Pay is experiencing a correlated growth.

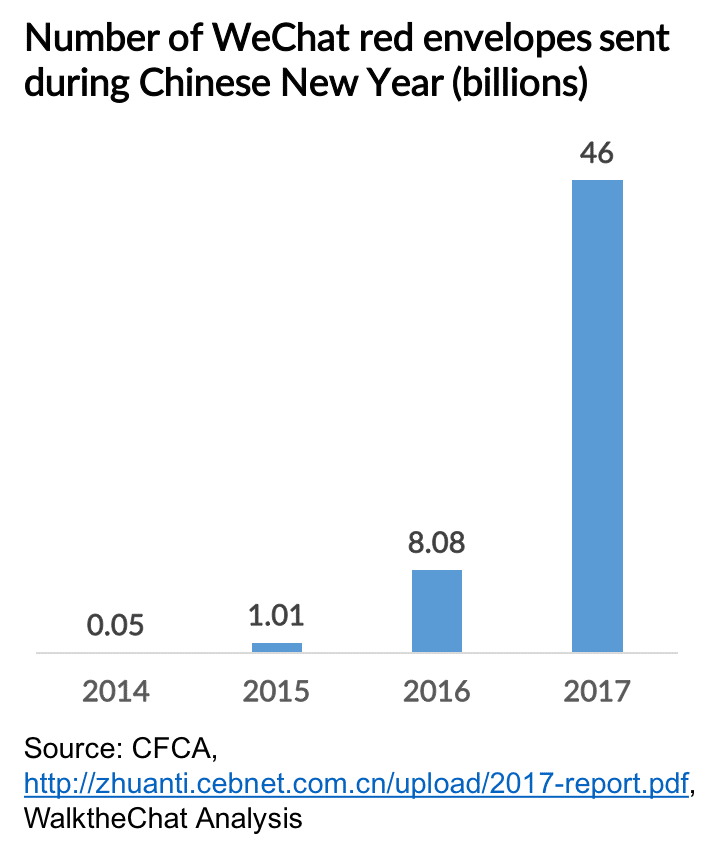

This growth was in no small part (as most readers might know already) due to the introduction of “digital red packets” during Chinese new year: this was the perfect combination of social and payment feature which pushed users to link their WeChat Account with their bank card.

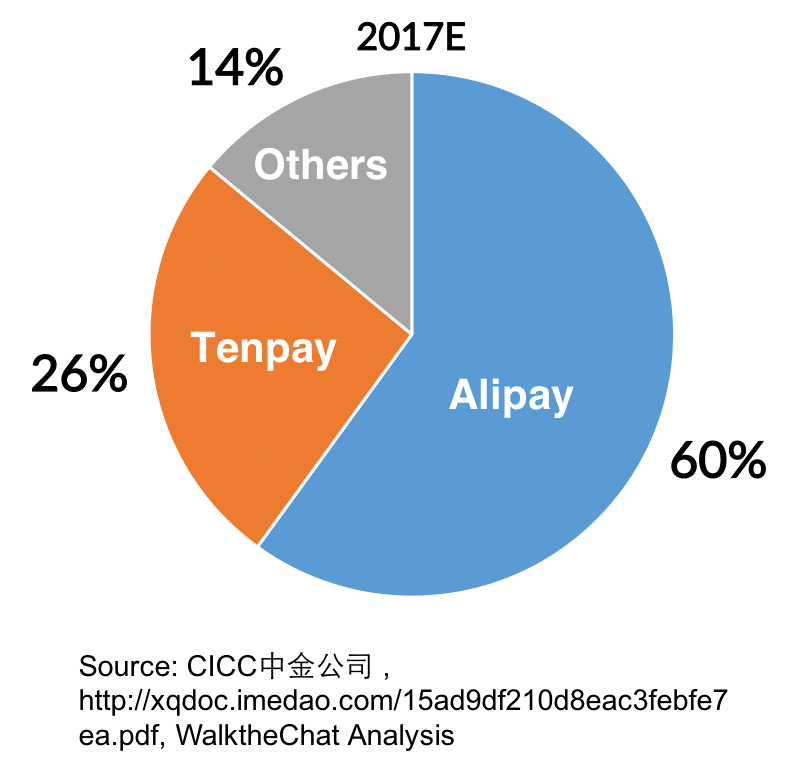

If WeChat is used more and more frequently, and might soon catch up with its rival when it comes to number of transactions, it remains behind when it comes to transaction volumes. This is mostly due to the large amount of transaction related to Taobao and Tmall, which still largely dominate the Chinese e-commerce landscape.

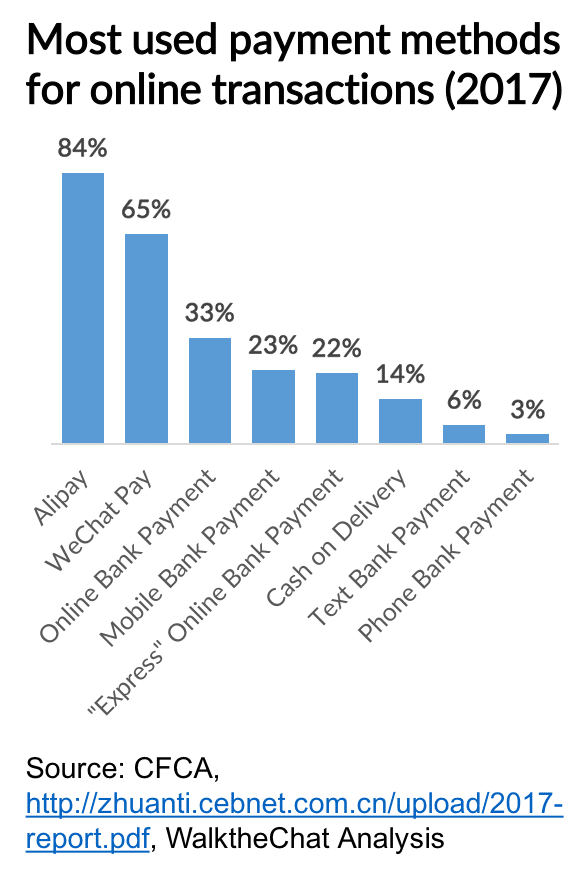

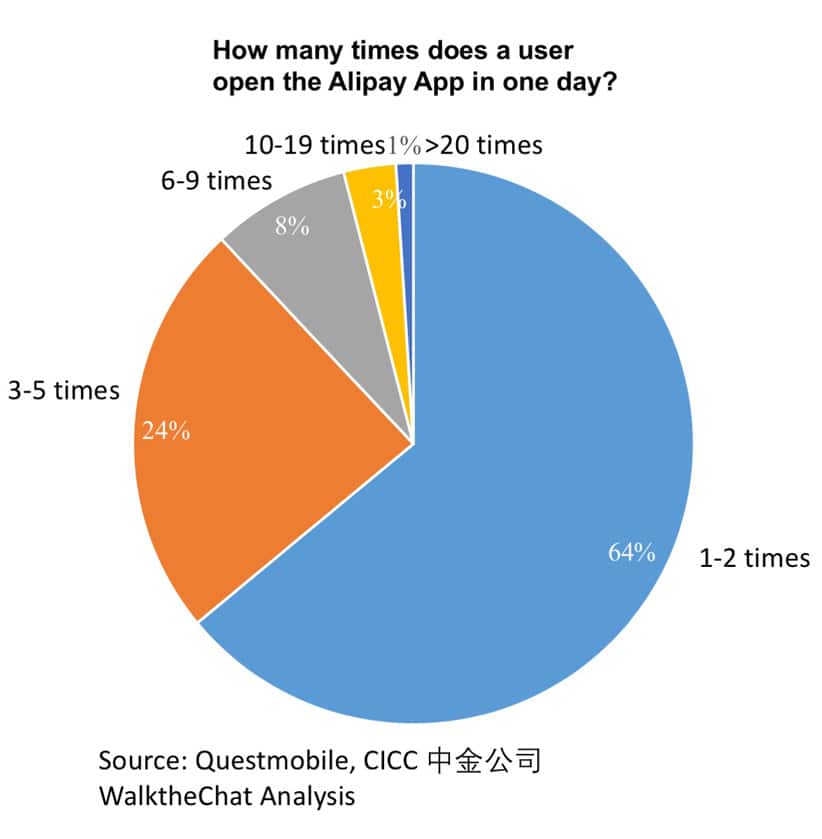

In terms of the frequency of use, WeChat is clearly ahead. User spend average of 66 minutes per day on WeChat in 2016, according to Quest Mobile. Total time spend on WeChat takes 35% of Chinese users’ daily phone usage. Comparatively, the average user only opens Alipay between 1-2 times per day. This high frequency usage gives WeChat a competitive advantage to become the most frequently used payment method, especially for offline transactions.

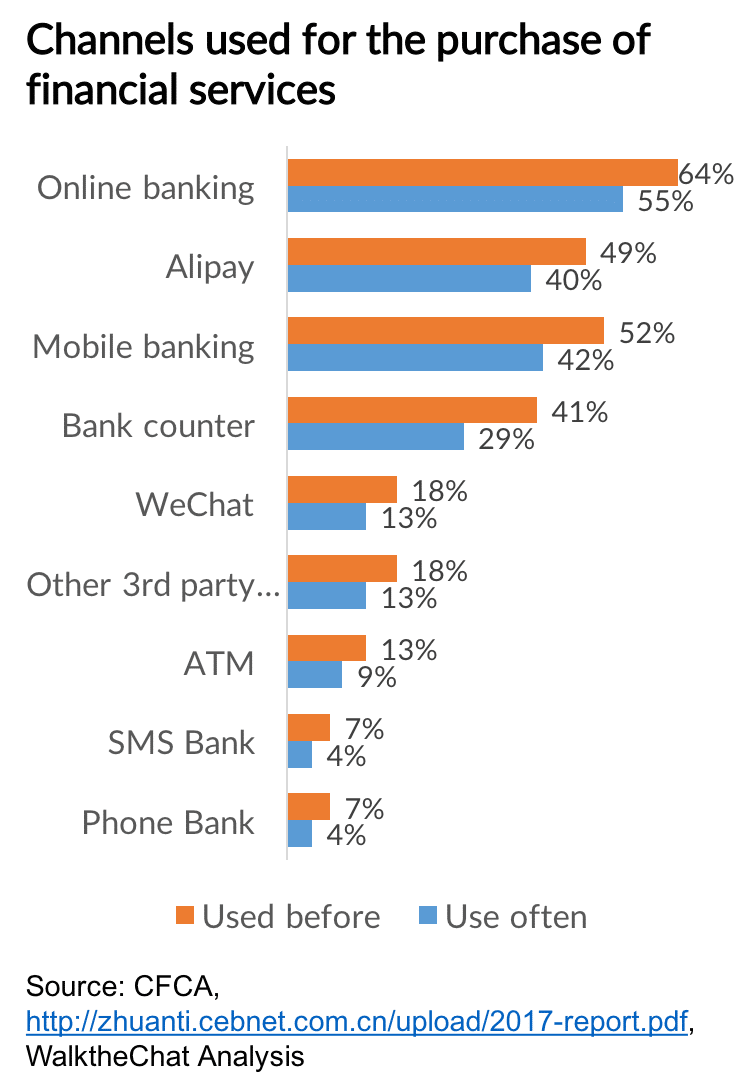

The social App also remains clearly behind Alipay (and its investment products Yue’Bao) when it comes to the purchase of financial services. Users are 3 times more likely to use Alipay as a tool for purchasing financial products.

Rising transaction fees

Both payment providers have been slowly but steadily including transaction costs. This started with WeChat starting to charge 0.1% on cumulative transfers over 20,000 RMB, which was then replaced by a 0.1% charge for all withdrawals (each user can withdraw only the first 1,000RMB with no charge) since Feb 2016.

Seven months later, Sep 2016, Alipay announced that due to rising operating costs, they will charge a 0.1% service charge to individuals who exceed the free transfer limit (20,000 RMB).

These measures have led to criticism from customers, especially while banks sometimes offer such transfer services free of charge.

Rising costs for WeChat and Alipay

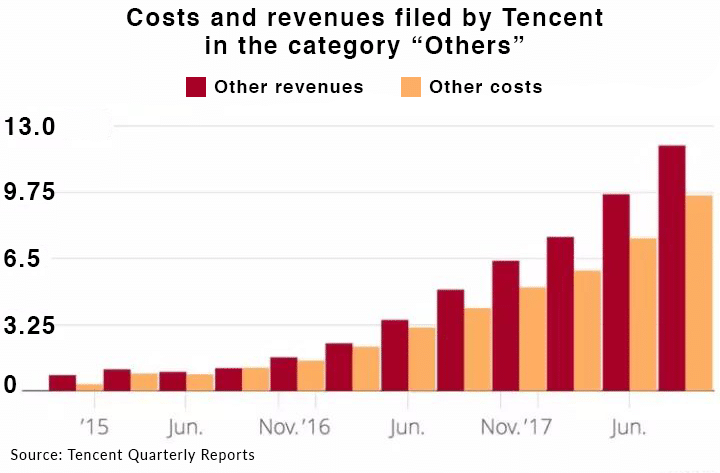

It is difficult to identify the costs of operation and revenues of WeChat Payment, as they are bundled together with their cloud computing services in the “Others” category of their annual reports.

The exponential growth of both costs and revenues of this category however suggests a growing impact of WeChat Payment (while Alibaba seems to be winning the cloud computing war)

Although the above graph suggests a profitable activity so far, things might change very soon.

Services like WeChat Pay and Alipay used to make large amounts of money through the “escrow” services of e-commerce platforms. When you purchase something on Taobao, the money isn’t sent directly to the merchant: it is held by Alibaba until you confirm the delivery. This creates a vast pool of money that Alibaba can invest and gain interests on.

According to a study conducted by CCTV Finance, these interest payments amounted to 7.1 billion yuan in 2016.

However, in April this year, the People’s Bank of China started imposing new requirements on the deposits obtained through escrow services, forcing them on accounts with lower or even no interest rates. This will surely impact the bottom line of payment companies, which may transfer some of these costs back to end users.

Conclusion

In the payment war, WeChat is quickly catching up with Alipay and might soon surpass it in terms of number of transactions (if not in terms of transaction volume). Both platforms are however being increasingly scrutinized and regulated. As the “wild west” of online payments is coming to an end, additional costs may surface for end users of both services.